Drowning in Credit Card Debt? How a Consolidation Personal Loan Cuts 42% Interest in 2026

You paid the “minimum due” again this month. It felt responsible. It wasn’t. On a credit card charging 3.5% a month, paying only the minimum can keep you in debt for years while interest quietly doubles what you borrowed. Millions of Indians are stuck in exactly this loop right now.

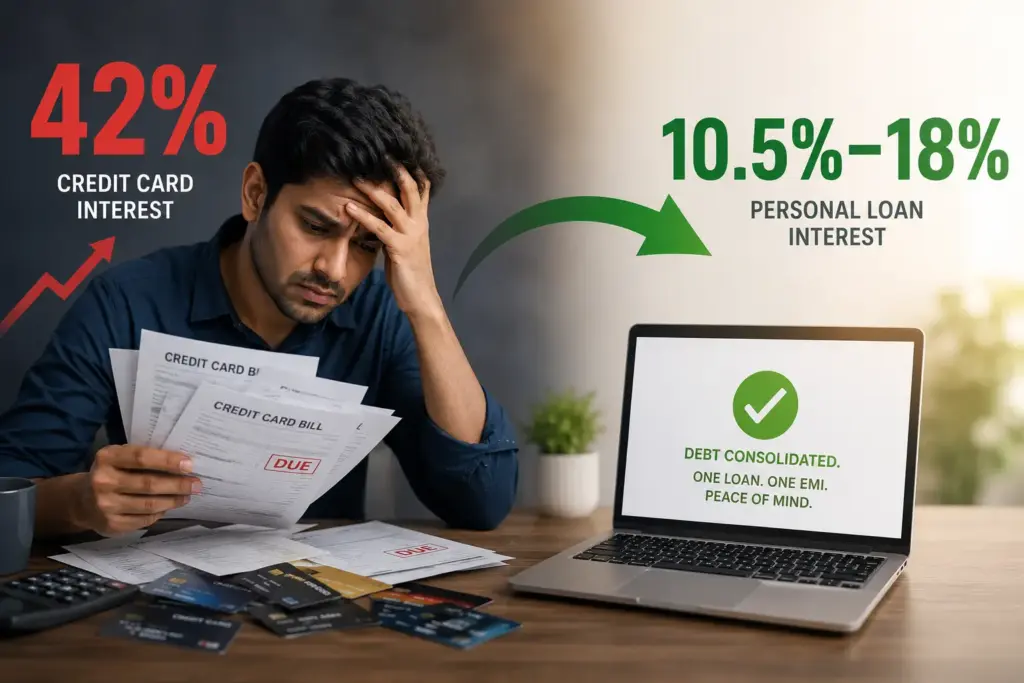

The numbers are alarming. India’s outstanding credit card debt reached ₹2.92 lakh crore by December 2024, and defaults jumped 28.42% year-on-year to ₹6,742 crore in the same period (OneIndia, RBI data, 2025). The trap is the interest rate: carry a balance past the interest-free window and a card can charge you up to 42% a year. There’s a way out that most people overlook, and it costs a fraction of that.

Key Takeaways

- Credit cards can charge up to 42% a year on carried balances, while a personal loan for debt consolidation typically costs about 10.5–18% (FinanceBuddha, 2026).

- A debt consolidation loan merges multiple card and loan dues into one personal loan with a single, lower EMI.

- On ₹1 lakh of debt, moving from ~42% to ~14% can save roughly ₹28,000 in a year of interest.

- Paying off cards on time with a consolidation loan can also help your CIBIL score over time, but only if you stop running up new card debt.

- A loan marketplace like SwipeLoan matches you to RBI-registered lenders so you can compare consolidation offers; the lender approves and disburses the loan.

Why Is Credit Card Debt So Dangerous?

Because the interest rate is brutal and the “minimum due” is designed to keep you paying it. A credit card that charges around 3.5% per month works out to roughly 42% a year on any balance you carry past the interest-free period (Business Standard, 2024). That’s two to four times what an unsecured personal loan costs.

The minimum-due trap makes it worse. Paying just 5% of your bill each month barely touches the principal, so interest keeps compounding on the rest. What looks like staying current is actually standing still while the debt grows underneath you.

This is why credit card debt behaves differently from other borrowing. A home or personal loan has a fixed end date, so you can see the finish line. Revolving card debt has no finish line by design; it renews every month you don’t clear it in full. Escaping it usually means converting that open-ended, high-rate balance into a closed-ended, lower-rate loan with a fixed payoff date.

What Is a Debt Consolidation Loan?

It’s a single personal loan you use to pay off several high-interest debts at once, most often credit card balances. Instead of juggling three or four cards with different due dates and 40%+ interest, you take one loan at a much lower rate, clear the cards, and repay that one loan in fixed monthly EMIs.

The mechanics are simple: the consolidation loan lands in your account, you immediately pay off every card, and you’re left with a single EMI at a single, lower rate. Consolidation loans in India typically run 1 to 7 years and can go up to ₹50–55 lakh depending on eligibility (Bajaj Finance, 2026).

According to lender data compiled in 2026, a personal loan used for debt consolidation generally carries an interest rate of about 10.5% to 18% a year for salaried borrowers with a reasonable credit profile (FinanceBuddha, Debt Consolidation Guide 2026). Against a card’s ~42%, that difference is the entire point.

For a full breakdown of how repayments are structured, see our guide to how personal loan EMIs and interest work.

How Much Can You Actually Save by Consolidating?

A lot. The gap between ~42% and ~14% is real money. Take a simple example: ₹1 lakh of credit card debt carried for a year. At a card’s ~42% annual rate, the interest alone is roughly ₹42,000. Move the same ₹1 lakh to a consolidation loan at ~14%, and the yearly interest drops to about ₹14,000, a saving of roughly ₹28,000 in a single year.

The saving grows with the balance. On ₹3–4 lakh of card debt spread across several cards, consolidating can free up thousands of rupees a month in interest. That’s money that was vanishing into finance charges. Just remember this is illustrative: your real rate depends on the lender’s credit policy and your profile.

Before you apply, use an EMI calculator to plan your consolidation and see what a single monthly payment would look like.

Does Consolidating Credit Card Debt Help or Hurt Your CIBIL Score?

It can help over time, if you use it correctly. Paying off your cards drops your credit utilisation ratio, one of the biggest factors in your score, and replacing several revolving balances with one loan you repay on time builds a positive record. Many borrowers see their score recover in the months after consolidating.

But it isn’t automatic. A new loan application triggers a hard enquiry, which can cause a small, temporary dip. And the benefit only holds if you don’t run the cards back up after clearing them. Consolidation cleans the slate; your spending habits decide whether it stays clean.

Our take: The single most common way debt consolidation fails is emotional, not financial. The moment those cards hit a zero balance, they feel like available money again. Treat consolidation as a one-way exit, not a reset button. Ideally, keep one card for genuine emergencies and pause the rest until the loan is cleared.

When Does Debt Consolidation NOT Make Sense?

When the maths or your habits don’t support it. Let’s be honest about that. Consolidation is a powerful tool, not a cure-all, and there are cases where it won’t help.

Think twice if:

- You’ll keep overspending. If you clear the cards and rack them up again, you end up with the loan and fresh card debt.

- Your balance is tiny. For a small amount you can clear in a month or two, processing fees may outweigh the interest saved.

- The new rate isn’t much lower. If a poor credit profile means you’re only offered a rate close to your card’s, the benefit shrinks, so check the numbers first.

- You’re considering settlement instead. “Settling” debt for less than owed damages your credit report far more than consolidating and repaying in full.

Run the comparison before you commit. If a lower-rate loan genuinely cuts your interest and you can hold your spending, consolidation is one of the smartest moves a borrower can make.

How Do You Get the Right Consolidation Loan?

Compare offers before you borrow. The rate gap between lenders decides how much you actually save. Two lenders can price the same borrower very differently, and on a multi-year loan even a couple of percentage points adds up.

A practical approach: add up everything you owe across cards and loans, then compare consolidation offers on three numbers: the interest rate, the processing fee, and the tenure that keeps your EMI affordable without dragging out total interest. The best offer is the one that lowers your rate meaningfully and fits a tenure you can comfortably repay.

This is where a marketplace saves you time. SwipeLoan is a credit-matching loan marketplace and Lending Service Provider under the RBI Digital Lending Guidelines 2022, not a lender. It matches you to a network of 100+ RBI-registered lending partners so you can compare debt consolidation offers in minutes. SwipeLoan doesn’t approve, price, or disburse the loan; that’s done by the partner lender under its own credit policy. Checking your options is a soft enquiry, so it has no impact on your credit score.

Trade a 42% credit card balance for a single, lower-rate EMI.

SwipeLoan is a credit-matching loan marketplace and Lending Service Provider (not a lender) that matches you to 100+ RBI-registered lending partners so you can compare debt consolidation loan offers side by side. Final rate, approval, and amount always depend on the individual lender’s credit policy; T&Cs apply.

Compare Consolidation Offers — Soft Check, No Score Impact →

Frequently Asked Questions

How do I get out of credit card debt in India?

The fastest structured way is a debt consolidation loan: a personal loan at about 10.5–18% a year that you use to pay off cards charging up to 42%. You clear all the cards at once, then repay a single EMI. Stopping new card spending is essential for it to work.

Is a personal loan cheaper than credit card debt?

Usually, yes, by a wide margin. Credit cards can charge around 42% a year on carried balances, while a personal loan for debt consolidation typically costs about 10.5–18% for a reasonable credit profile (FinanceBuddha, 2026). The exact rate depends on the lender and your profile.

Will debt consolidation improve my CIBIL score?

It can, over time. Paying off cards lowers your credit utilisation, and repaying one loan on time builds a positive record. But the initial application causes a small, temporary dip, and the benefit only holds if you don’t build new card debt afterward.

How much debt can I consolidate with a personal loan?

Consolidation personal loans in India can go up to ₹50–55 lakh depending on your income and eligibility, with tenures of 1 to 7 years (Bajaj Finance, 2026). The approved amount is decided by the lender based on its credit policy.

Does SwipeLoan give consolidation loans directly?

No. SwipeLoan is a credit-matching loan marketplace and Lending Service Provider that connects you to RBI-registered banks and NBFCs. Every loan is approved and disbursed by the partner lender, subject to that lender’s credit policy and T&Cs.

Conclusion

Credit card debt is expensive by design. The minimum due keeps you comfortable while 42% interest keeps you stuck. A consolidation personal loan breaks that loop by swapping an open-ended, high-rate balance for a fixed, lower-rate one with a real payoff date.

The move only works if you do two things: get a rate meaningfully below your card’s, and stop reaching for the cards once they’re clear. Add up what you owe, compare a few RBI-registered lenders, and pick the offer that lowers your rate without stretching your budget. Do that, and the debt that felt permanent gets an expiry date.